You can start investing with as little as $5 right now. That’s not a gimmick or a clickbait headline—it’s the reality of investing in 2026. I remember sitting on my couch five years ago with exactly $43 in my “extra” money pile, convinced I needed at least a thousand to bother. I was wrong. Dead wrong. And honestly? I’m still a little annoyed at how many years I wasted thinking that way.

Whether you’ve got twenty bucks or two hundred, the market doesn’t discriminate. It just rewards consistency. So let’s cut through the noise and talk about how regular people—with regular paychecks and regular bills—can actually build something.

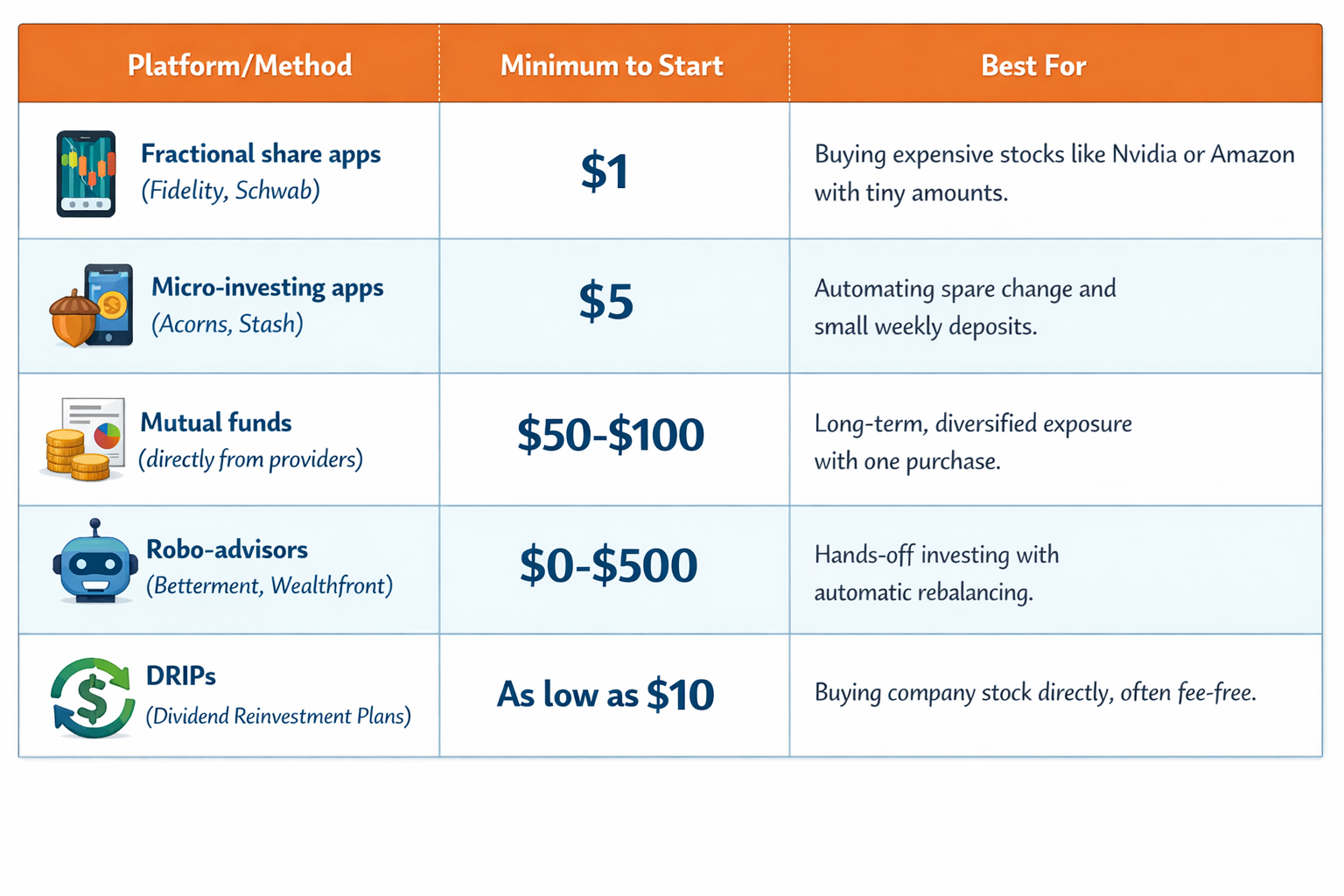

What’s the Minimum Money Needed to Start Investing?

The short answer: as low as $1 to $100, depending on where you go.

Here’s the breakdown based on current platforms (2025-2026):

Real talk: I opened my first account with $43. It felt embarrassing. But that $43 turned into automated weekly $10 deposits, and those turned into real growth over time. The amount matters less than the habit.

5 Simple Ways to Start Investing With Small Money

1. Buy Fractional Shares (The Game Changer)

Fractional shares are exactly what they sound like—you buy a slice of a stock instead of a whole share.

Example: As of early 2026, one share of Berkshire Hathaway Class A costs around $600,000. Absurd, right? But you can buy $25 worth through fractional shares. You own a tiny piece of Warren Buffett’s empire for the price of dinner.

How to do it:

- Open a brokerage account at Fidelity, Schwab, Robinhood, or M1 Finance

- Search for the company you want

- Enter the dollar amount you want to invest ($5, $10, whatever)

- Hit buy. That’s it.

2. Automate With Micro-Investing Apps

This is the “set it and forget it” method that actually works. Apps like Acorns connect to your debit card, round up purchases to the nearest dollar, and invest the difference.

Real scenario from last week: My coffee was $4.50. The app rounded up to $5 and invested $0.50. By Friday, I had $12 in micro-investments without noticing.

Current trend (2026): These apps now offer “bonus rounds” where they match a percentage of your round-ups during certain months. It’s small, but free money is free money.

3. Start With a Low-Minimum Mutual Fund

Mutual funds are the original small investor tool, and they’re still one of the best. Instead of picking individual companies, you own a basket of them. When people ask me where to put their first $100, I almost always point them toward a good mutual fund. Why? Because mutual funds give you instant diversification without requiring you to be a stock-picking genius. A single mutual fund can hold hundreds or even thousands of companies, which means if one crashes, your whole mutual fund doesn’t implode.

Personal experience: My first real Investment Plan was $100/month into an S&P 500 index fund (which is a type of mutual fund). Boring? Absolutely. But over five years, that boring mutual fund grew faster than my “exciting” stock picks. The mutual fund averaged 10-12% annually while I stressed over individual stocks that went nowhere. That’s the power of a solid mutual fund in a long-term Investment Plan.

Best low-minimum mutual funds right now (2026):

- Fidelity ZERO Total Market Index Fund (FZROX) – $0 minimum

- Schwab S&P 500 Index Fund (SWPPX) – $100 minimum

- Vanguard Target Retirement Funds – $1,000 minimum

4. Join a Dividend Reinvestment Plan (DRIP)

This is old-school but brilliant. Many companies let you buy stock directly from them, often with low fees or no fees. Then, any dividends the company pays automatically buy more shares.

Why I like this for small investors: It forces compound growth. You’re not just owning stock; you’re using the dividends to buy more stock, which creates more dividends. It’s a snowball effect.

Example: Procter & Gamble (PG) has paid dividends for 134 consecutive years. If you buy $50 worth through their DRIP, you’re automatically enrolled in that history.

5. Use a Robo-Advisor for Hands-Off Growth

If you don’t want to think about it at all, robo-advisors are your answer. You answer a few questions about your goals and risk tolerance, and an algorithm builds and manages a portfolio for you.

Current 2026 update: Most robo-advisors now offer “direct indexing” for smaller accounts, meaning they buy the actual stocks in an index rather than a fund, which can be more tax-efficient. Betterment and Wealthfront lead here.

How to Build a Realistic Investment Plan With Low Money

An Investment Plan doesn’t need to be complicated. In fact, the best Investment Plan is usually the simplest one you’ll actually stick with. I’ve tried fancy Investment Plan strategies with spreadsheets and allocation targets, and you know what happened? I abandoned them in three months.

Here’s exactly what I tell friends who ask me how to start their first Investment Plan:

Step 1: Pick Your Platform

Choose one of the options above based on your comfort level. For absolute beginners, I usually recommend:

- Acorns if you want pure automation

- Fidelity if you want control and fractional shares

- Betterment if you want hands-off management

Step 2: Set a Recurring Amount

Decide what you can afford weekly or monthly. Be honest. $10 a week is $520 a year. $20 a week is $1,040. It adds up. A solid Investment Plan doesn’t require huge amounts—it requires consistency.

My rule: Start smaller than you think you can handle. It’s better to consistently invest $10 than to invest $100 once and quit. Your Investment Plan should feel almost boring, not stressful.

Step 3: Automate It

Set up automatic transfers from your bank to your investment account on payday. This is non-negotiable. If you have to manually move the money, you’ll eventually skip a week. The best Investment Plan in the world fails if you don’t actually fund it.

Step 4: Choose What to Buy

For the first year, I’d suggest:

- 80% in a broad market mutual fund or ETF (like VTI or FZROX)

- 20% in something you find interesting (a stock you believe in, a sector ETF, etc.)

This keeps you diversified but also gives you skin in the game and keeps you engaged. Remember, mutual funds should be the foundation of your Investment Plan because they spread risk across dozens or hundreds of companies.

Step 5: Ignore It (Mostly)

Check your account once a month at most. Obsessing daily will drive you crazy and tempt you to make stupid decisions during market dips. A good Investment Plan works in the background while you live your life.

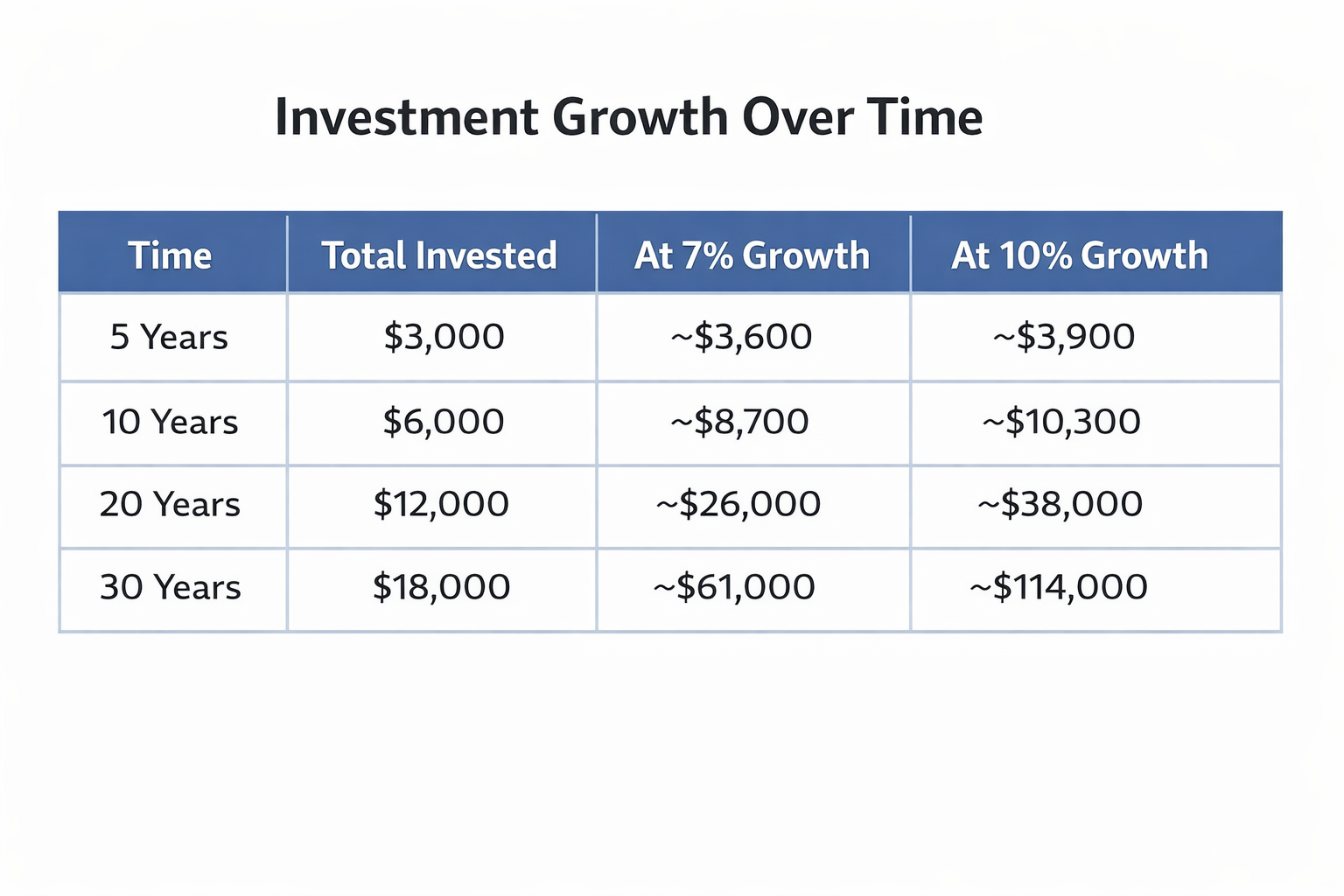

Real Numbers: What $50/month Looks Like Over Time

Let’s do the math that finally convinced me to stop waiting:

That’s $50/month. The cost of Netflix and a coffee run.

The catch: You have to actually do it and leave it alone. The people who fail are the ones who panic-sell when the market drops 10% or cash out for an “emergency” that wasn’t really an emergency.

Common Mistakes I Made (So You Don’t Have To)

Mistake 1: Waiting for the “Perfect” Amount

I waited until I had $1,000 saved. Then the car needed repairs. Then it was the holidays. I waited two years. Missed a 25% market run. Start with what you have now. Your first Investment doesn’t need to be impressive—it just needs to happen.

Mistake 2: Picking “Exciting” Stocks Over Boring Funds

I bought a hot tech stock because a friend swore it would moon. It didn’t. Lost 40%. Meanwhile, my boring mutual fund kept chugging along. Lesson learned. When I rebuilt my Investment Plan, I made sure mutual funds were the core. Mutual funds aren’t sexy, but mutual funds also don’t keep you up at night wondering if you’ll lose everything.

Mistake 3: Checking the App Every Hour

This is just self-inflicted anxiety. The market moves up and down daily. Over years, it trends up. Stop looking. Every time I ignored my Investment for a few months, I came back to pleasant surprises.

Mistake 4: Not Having a Real Plan

I invested randomly—$50 here, $20 there, skipping months. When I finally set up automatic weekly buys, my account started actually growing. Consistency beats intensity. A real Investment Plan removes the guesswork and emotion.

What About Current Trends?

A few things happening right now that small investors should know:

AI trading bots are everywhere. Apps now offer AI-powered suggestions based on your spending patterns. Use them as guidance, not gospel. They’re helpful for identifying cash you can redirect to Investment, but they’re not fortune tellers.

Fractional crypto is expanding. If you’re curious about crypto but scared of the volatility (smart), most apps now let you buy $1 fractions of Bitcoin or Ethereum. I keep about 5% of my small portfolio here, but I sleep fine knowing it’s money I can lose.

ESG investing is maturing. Environmental, Social, and Governance funds used to be marketing fluff. Now, many have competitive returns and low minimums. If you want your Investment to align with your values, you can start with $50 in funds like ESGV or SUSA.

High-yield savings are actually decent again. With rates hovering around 4-5% in 2026, it’s worth keeping your emergency fund in one of these while you invest the rest. Ally, Marcus, and SoFi are solid.

Conclusion: Start Your Investment Journey Today

Look, I’ve been where you are. I’ve stared at my bank account, done the mental math, and convinced myself I’d start “next month” or “when I get that raise” or “after the holidays.” And every time I did that, I lost time I’ll never get back.

Here’s what I’ve learned after years of watching friends succeed and fail with money: the people who build wealth aren’t the ones who made the most money. They’re the ones who started early and stayed consistent. They put $20 a week into a mutual fund and forgot about it. They built an Investment Plan that worked automatically. They treated Investment like a bill—non-negotiable, due every month.

You don’t need to be rich to invest. You don’t need to understand options trading or read earnings reports. You just need to start. Put $10 in a mutual fund this week. Set up that automatic transfer. Buy that fractional share. The amount doesn’t matter as much as the act.

Because here’s the secret nobody tells you: once you make that first Investment, something shifts. You stop being someone who “wants to invest” and become someone who actually does. And that identity shift—that tiny mental flip—is worth more than any stock tip I could give you.

So open the app. Put in the money. Buy the mutual fund. Start the Investment Plan. Future you is going to be so glad you did.

Frequently Asked Questions About Investment With Low Money

What is the best way to start investment with low money?

The best way to start investment with low money is through SIP-based mutual funds. They allow beginners to invest small amounts regularly, spread risk across multiple assets, and grow wealth over time without needing deep market knowledge.

Can beginners invest with low money without taking high risk?

Yes, beginners can invest with low money without taking high risk by choosing diversified options like mutual funds and simple investment plans. Starting small and investing consistently helps reduce risk while building confidence and experience.

How much money do I need to start investing for the first time?

You can start investing with a very small monthly amount using beginner-friendly investment plans such as SIPs. Many people begin with low money and gradually increase their investment as their income and confidence grow.

Are mutual funds suitable for low-money investment?

Yes, mutual funds are suitable for low-money investment because they diversify your money across different companies and are professionally managed. This makes them a practical and reliable option for beginners looking for long-term growth.