If you are searching for “what are gilt funds,” chances are you want to invest safely. Maybe you have seen market volatility and feel nervous.

I completely understand that feeling.

In this guide, I will explain gilt funds in India in simple English. No complex jargon. Just real talk from experience.

By the end, you will know if these government bond funds belong in your portfolio.

What Exactly Are Gilt Funds?

Let me break this down.

Gilt funds are a type of debt mutual fund that invests only in government securities.

Think of it like this: You are lending money to the Government of India. In return, the government pays you interest on time. And at maturity, they return your principal.

That is why many call them the safest mutual funds in the country. The government has never defaulted on local currency debt.

Short answer for beginners: Gilt funds = mutual funds that hold only central and state government bonds.

How Do Gilt Funds Work in Real Life?

Here is an example from the Indian market.

Imagine a gilt fund buys a 10-year government bond with a 7.2% interest rate. The fund earns that interest. But here is the catch most beginners miss.

The price of that bond changes daily.

Why? Because interest rates move up and down. When RBI changes rates, your bond’s market value moves.

From my experience: Many beginners buy gilt funds thinking they are like fixed deposits. They are not. Your principal can go down in the short term even though the government never defaults.

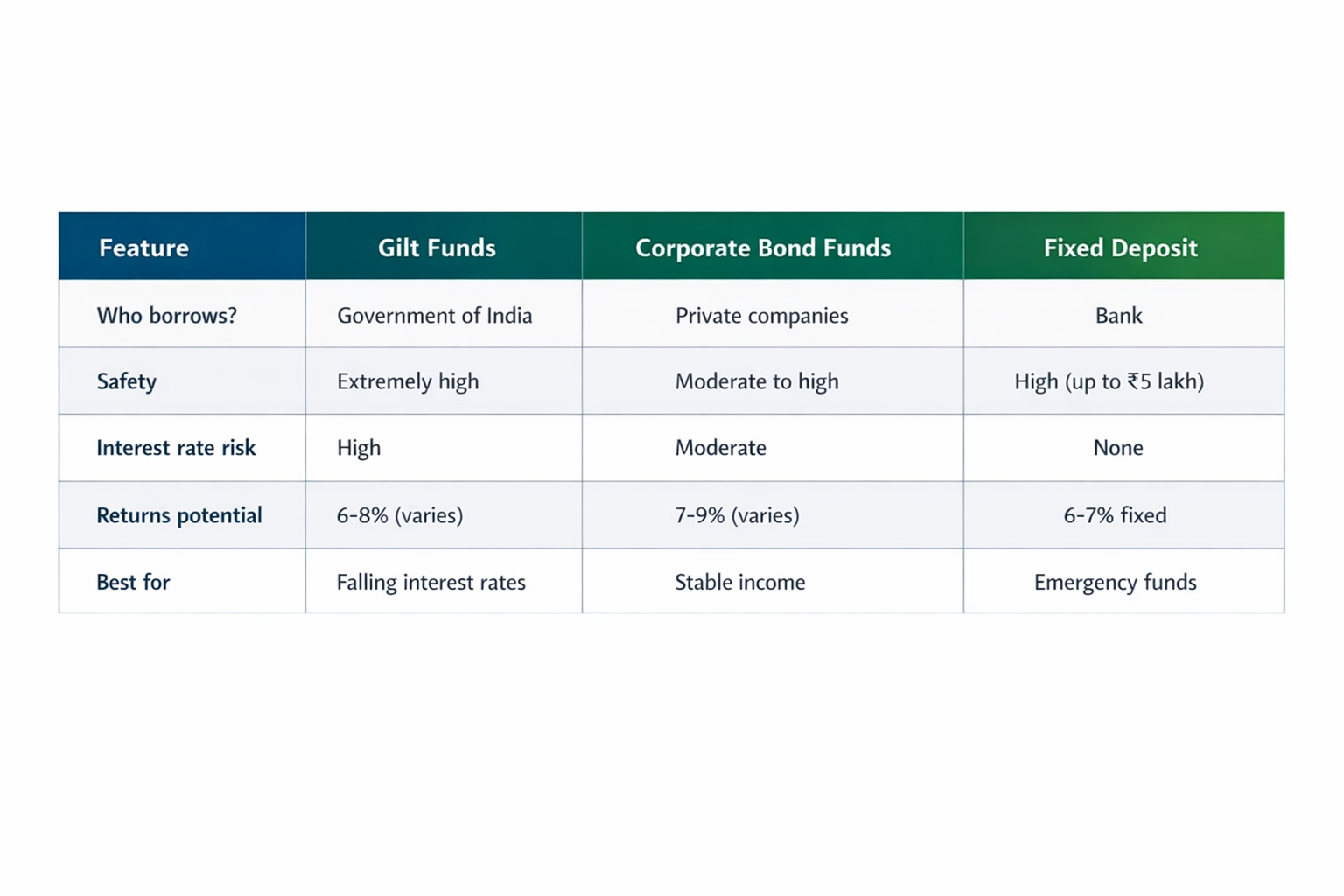

Gilt Funds in India vs Other Debt Funds

This table will save you hours of confusion.

Pro tip: Do not compare gilt funds with FDs directly. They behave very differently.

When Should You Invest in Gilt Funds?

Here is where experience matters.

From my years of investing, gilt funds perform best in one specific scenario: when interest rates are expected to fall.

The Logic Behind It

Suppose RBI cuts interest rates from 6.5% to 6%.

- Old bonds paying 7% become more valuable.

- Their prices go up.

- Your gilt fund NAV rises.

Real-world India context: In 2024-2025, when RBI signaled rate cuts, gilt funds delivered double-digit returns in just a few months. But when rates rise, these funds can lose 4-5% quickly.

A Common Beginner Mistake

Many new investors see “government-backed” and assume zero risk. Then they panic when their ₹1 lakh becomes ₹96,000 in a rising rate environment.

Warning from experience: Gilt funds have high interest rate risk. Do not invest money you need within 2-3 years.

The Two Biggest Risks in Gilt Funds

Let me be completely transparent.

1. Interest Rate Risk

This is the main risk.

When interest rates go UP → bond prices go DOWN → your gilt fund value drops.

Example: In 2022, when RBI started hiking rates, many gilt funds fell 5-6%. Investors who panicked sold at a loss.

2. Duration Risk

Duration measures how sensitive your fund is to rate changes.

- Longer duration = higher volatility

- Short-term gilt funds exist but are rare

What I tell my friends: If you cannot handle a 5-7% temporary drop, avoid long-duration gilt funds.

Who Should Actually Buy Gilt Funds?

Not everyone needs gilt funds. Here is my honest take.

Good for:

- Investors with a 5+ year horizon

- Those expecting falling interest rates

- Portfolio diversification (small allocation)

- Conservative investors who still want better than FD returns

Not good for:

- Emergency funds (use liquid funds or savings account)

- Short-term goals under 3 years

- Anyone who panics seeing red numbers

From my experience: A 10-15% allocation to gilt funds makes sense for aggressive investors. For conservative investors, maybe 20-30%. But never 100%.

How to Choose the Best Gilt Fund in India

Follow these 5 steps.

- Check expense ratio – Lower is better (under 1% is good)

- Look at duration – Choose based on your risk appetite

- See AUM size – Over ₹500 crore is safer

- Track record – How did the fund perform in 2022 rate hikes?

- Exit load – Some funds charge for early exit

Popular options to research (not advice): SBI Gilt Fund, ICICI Prudential Gilt Fund, HDFC Gilt Fund.

Pro Tips for Gilt Fund Investing

Here are lessons from my real mistakes.

Tip 1: Never lump sum before an RBI policy meeting. Wait for clarity.

Tip 2: Use SIPs in gilt funds to average out interest rate cycles.

Tip 3: Watch the 10-year G-sec yield. When it is high (above 7.2%), gilt funds become attractive.

Tip 4: Do not check NAV daily. Interest rate risk creates noise. Check monthly.

Tip 5: Combine with corporate bond funds for better risk-reward balance.

Small Data Point to Remember

Historically, gilt funds in India have delivered 7-9% returns over full interest rate cycles (5-7 years). But within that, you may see -5% one year and +12% another year.

That volatility is normal. Do not panic.

Conclusion: Are Gilt Funds Right for You?

Let me summarize clearly.

Gilt funds are among the safest mutual funds in terms of default risk. But they come with interest rate risk. They are not like bank FDs.

If you understand rate risk and have a long horizon, they can be a great addition. If you want predictable returns with no volatility, stick to FDs or liquid funds.

My final advice: Start small. Maybe ₹2,000-5,000 per month via SIP. Observe how price changes feel. Then decide.

Investing is not about being right. It is about staying comfortable enough to not sell at the wrong time.

Frequently Asked Questions

1. Are gilt funds risk-free?

No. They have no default risk because the government backs them. But they have high interest rate risk. Your NAV can go down when rates rise.

2. Can I lose money in gilt funds?

Yes, in the short term. If you sell when interest rates have risen, you can absolutely lose principal. Over 7+ years, losses are rare.

3. What is the difference between gilt funds and G-secs?

G-secs are individual government bonds. Gilt funds are mutual funds that hold many such bonds. Funds offer diversification and professional management.

4. Are gilt funds tax-free?

No. They are taxed like debt funds. Short-term (under 3 years) – as per income tax slab. Long-term – 20% with indexation benefit.

5. When is the best time to buy gilt funds?

When RBI is about to cut interest rates or when 10-year G-sec yields are near peak levels. Avoid buying when rates are already falling for a long time.

6. Are gilt funds safe for senior citizens?

Partly. They are safe from default but volatile. Senior citizens needing regular income may prefer senior citizen savings scheme or monthly income plans instead.

7. How are gilt funds different from corporate bond funds?

Gilt funds invest only in government securities. Corporate bond funds invest in company debt. Gilt funds are safer but often more volatile to interest rate changes.

8. What is the minimum investment in gilt funds?

Usually ₹500 or ₹1,000 for lump sum. SIPs can start as low as ₹500 per month. Check individual fund documents.

9. Do gilt funds pay dividends?

Some offer dividend options. But from a tax perspective, growth option is usually better. Dividends are not guaranteed.

10. Can gilt funds give negative returns in a year?

Yes. In rising rate years like 2022, many gilt funds gave negative returns. But over 5+ years, most recover and deliver positive returns.