Introduction

Are you looking for a best investment plan for monthly income in 2026? You are not alone. With the rising cost of living and the desire for financial freedom, more Indians are shifting from saving money to generating passive income.

In 2026, the financial markets offer a mix of safe investment plans and market-linked options. Gone are the days when you had to rely only on your salary or pension to pay the bills. Today, you can create a regular monthly income stream using Mutual Funds SWP, Fixed Deposits, Government Schemes, and even Real Estate.

However, choosing the right monthly income plan is tricky. High returns often come with high risk, while safe options might not beat inflation.

In this detailed guide, we will cover the top 5 investment options for monthly income in 2026, their expected returns, risk levels, tax implications, and a comparison table to help you decide which plan fits your financial goals. Whether you are a retiree, a salaried employee, or a young investor, this article will help you build a passive income portfolio that aligns with the latest Google Core Update standards for quality content.

Why Monthly Income Investments Are Important in 2026

Rising Cost of Living and Inflation

Inflation remains a silent killer of wealth. In 2026, while the RBI has managed to keep core inflation in check, the cost of daily essentials, healthcare, and education continues to rise. If your money is sitting idle in a regular savings account (offering 2.5% to 3% interest), you are losing purchasing power every year. You need investment plans for monthly income that generate at least 7-8% returns to keep up with the rising cost of living.

Need for Passive Income Sources

Job stability is no longer guaranteed. Whether you are a salaried employee or a freelancer, having a second source of income—specifically passive income—provides a financial safety net. A monthly income plan ensures that even if your paycheck stops, your expenses are covered. In 2026, digital tools have made it easier to track SWPs and dividends, making passive income accessible to the middle class .

Best Investment Options for Salaried Employees and Retirees

Your risk profile changes with age.

- For Salaried Employees (25-50 years): You can afford moderate risk for higher tax-efficient returns. Options like SWP in Hybrid Mutual Funds or Dividend Stocks suit you.

- For Retirees (60+): Capital protection is paramount. Senior Citizen Savings Scheme (SCSS) and Post Office Monthly Income Scheme (POMIS) are the safest bets .

How AI and Digital Platforms Changed Investing in 2026

Technology has revolutionized investing. In 2026, AI-driven robo-advisors analyze your spending habits and automatically invest surplus funds into debt or equity to generate income. Moreover, platforms now allow you to start a Systematic Withdrawal Plan (SWP) with just a few clicks, offering instant liquidity and precise control over your monthly cash flow .

Things to Check Before Choosing a Monthly Income Investment Plan

Before you put your hard-earned money into any plan, you must check these five parameters to avoid losses.

Risk vs Return

This is the golden rule. High returns = High risk. If a plan promises 12% monthly income, it is likely a scam or a very high-risk instrument like P2P lending. Government schemes offer 7-8% with zero risk, while stocks offer 10-12% with volatility.

Liquidity and Withdrawal Options

What if you need the money urgently? Fixed Deposits and SCSS have lock-in periods; breaking them early may incur a penalty (e.g., POMIS deducts 1-2% for early withdrawal) . Mutual Fund SWPs offer high liquidity—you can stop the withdrawal and redeem the entire amount the next business day.

Tax Benefits and Taxation Rules

In 2026, taxation is a major deciding factor.

- FDs and Schemes: Interest is added to your income and taxed as per your income slab (up to 30%).

- SWP in Debt Funds: Taxed as capital gains. Indexation benefit applies if held for over 3 years, making it tax-efficient for high-income earners .

- Dividends: Taxable in the hands of the investor.

Investment Duration

How long can you stay invested?

- Short-term (1-3 years): Go for Bank FDs or Short-term Debt Funds.

- Long-term (5+ years): SCSS, POMIS, or Real Estate are better.

Monthly Income Stability

Do you need a guaranteed monthly income or a variable one? Government schemes give you a fixed amount. SWPs give a fixed amount but the principal fluctuates with the market.

Top 5 Investment Plan for Monthly Income in 2026

Let us dive into the core list of the five best investment avenues available to Indian investors right now.

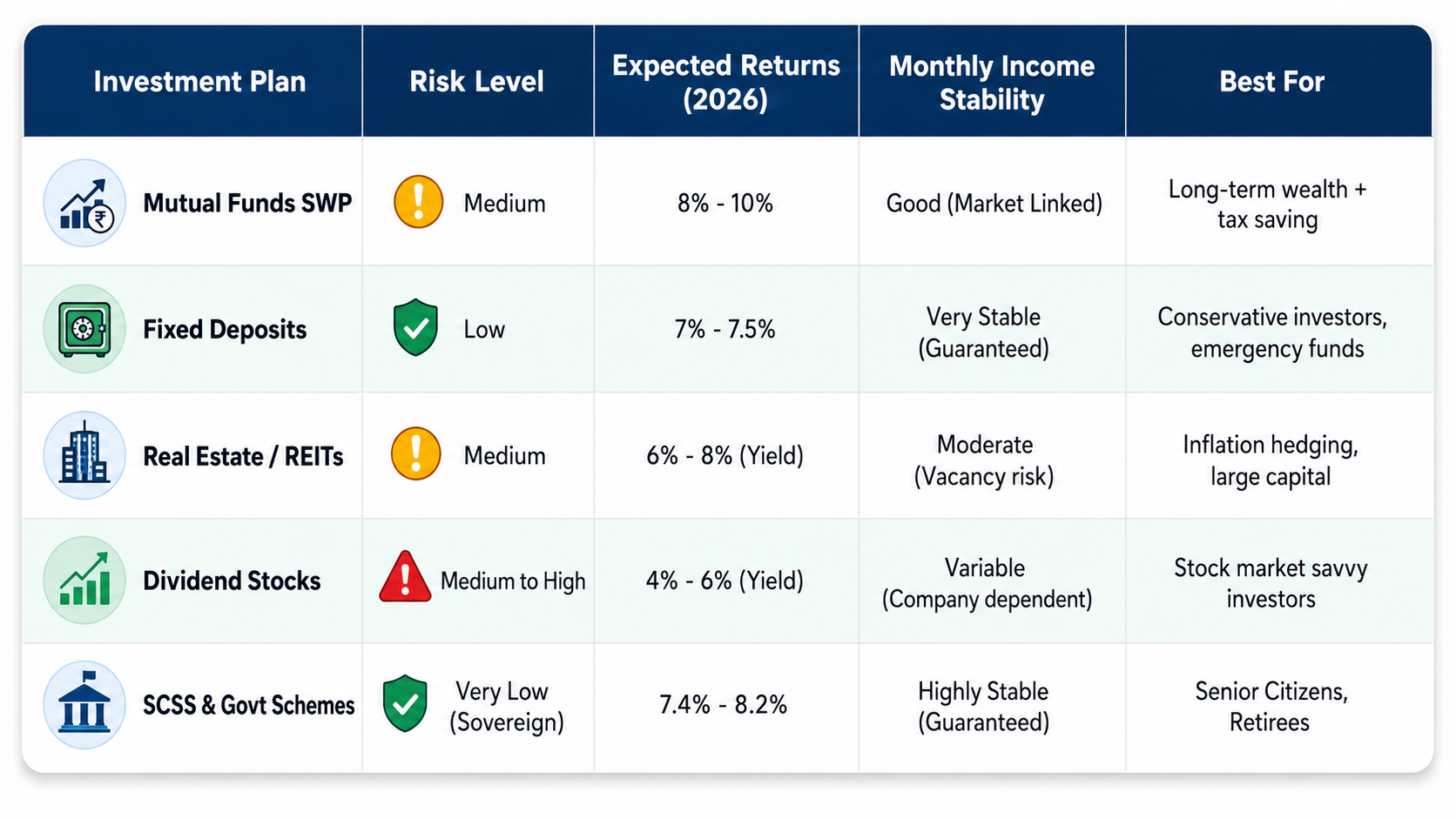

1. Mutual Funds with SWP (Systematic Withdrawal Plan)

What is SWP in Mutual Funds?

SWP is the modern way to generate income. Instead of receiving a dividend (which the company decides), you decide how much money you want to withdraw from your mutual fund every month. You invest a lump sum amount (say ₹20 lakh) into a mutual fund. The fund grows over time. You instruct the fund to send you ₹15,000 every month. This is called Systematic Withdrawal Plan .

Expected Monthly Income and Returns in 2026

In 2026, conservative hybrid funds (debt + equity) are expected to return 8-10% annually. Using an SWP calculator, if you invest ₹10 lakh, you can safely withdraw about ₹6,000 to ₹7,000 per month without depleting the principal for a long time.

Benefits of SWP Investment Plans

- Tax Efficiency: You only pay tax on the capital gains portion of the withdrawal, not the entire amount. This is much better than FD interest which is fully taxed .

- Flexibility: You can change the withdrawal amount or stop it anytime.

- Rupee Cost Averaging in Reverse: When markets are down, you sell fewer units; when markets are up, you sell more units.

Risks of Mutual Fund Investments

SWP does not guarantee capital protection. If the stock market crashes for a prolonged period, your withdrawals will eat into your original capital. It is suitable only for those with a moderate risk appetite.

Best For Long-Term Investors

Best for: Individuals under 50 looking to retire early or supplement their salary.

Recommended Funds (for research): ICICI Prudential Balanced Advantage Fund, SBI Equity Hybrid Fund .

Recommended Funds (for research): ICICI Prudential Balanced Advantage Fund, SBI Equity Hybrid Fund .

Suggested SEO Keywords Naturally: Monthly income mutual funds, best SWP plans 2026, passive income investment, tax free monthly income.

2. Fixed Deposits (FDs) with Monthly Interest Payout

How Monthly Interest FD Works

A Fixed Deposit is the traditional safe haven. While standard FDs pay interest at maturity, you can choose a “Non-Cumulative” FD option. This pays you interest every month directly into your bank account. The principal amount remains untouched and is returned to you at the end of the tenure.

Latest FD Interest Rates in 2026

As of mid-2026, top banks (SBI, HDFC, ICICI) offer senior citizens up to 7.5% – 8.0% and general citizens 7.0% – 7.25% on 1-3 year tenures. Small finance banks (like AU, YES Bank) offer slightly higher rates (up to 8.5%) for monthly payouts .

Benefits of Fixed Deposit Investments

- Guaranteed Returns: You know exactly how much you will get each month.

- Safety: Up to ₹5 lakh is insured by DICGC.

- Simplicity: Easy to open via net banking.

FD vs Savings Account

A savings account gives you 2.7% – 3% interest. A monthly income FD gives you 7%+. The trade-off is liquidity; breaking an FD early costs a penalty (usually 1%).

Best Banks for Monthly Income FDs

- HDFC Bank: Offers 7.2% for seniors (Monthly Payout).

- Post Office Time Deposit: 6.9% – 7.1% (Quarterly compounded, but monthly payout possible via MIS).

- Small Finance Banks: High rates but moderate risk.

Suggested SEO Keywords: Best FD plans 2026, monthly income fixed deposit, safe investment plans, guaranteed monthly income.

3. Real Estate Rental Income

Why Rental Properties Still Work in 2026

Despite high property prices, real estate remains a favorite for passive income because it acts as an inflation hedge. When inflation rises, rents rise too. In 2026, the demand for commercial office space and warehousing has surged, providing high rental yields.

Residential vs Commercial Property Investment

- Residential: Lower yield (2% – 3% of property value annually), but stable demand.

- Commercial (Shops/Offices): Higher yield (6% – 8% annually), but vacancy risk is higher.

- Alternative: REITs (Real Estate Investment Trusts). If you don’t have ₹50 lakh to buy a property, you can buy REIT units on the stock exchange for as low as ₹1,000. They distribute 90% of their rental income to unitholders .

Rental Yield Explained

If a property costs ₹1 crore and you earn ₹40,000 rent per month, your annual yield is 4.8%. In 2026, Tier-2 cities are offering better yields than Tier-1 metros due to lower property costs.

Risks in Real Estate Investments

- Illiquidity: You cannot sell a property in 1 day.

- Maintenance: Painting, repairs, and dealing with tenants requires effort.

- Vacancy: No tenant means no income.

Tips to Generate Stable Rental Income

- Location is King: Buy near IT parks, colleges, or hospitals.

- REITs: If you hate managing tenants, switch to REITs like Embassy Office Parks REIT .

Suggested SEO Keywords: Real estate investment 2026, rental income ideas, property investment for monthly income, how to earn passive income from property.

4. Dividend Paying Stocks

What Are Dividend Stocks?

When companies (like Hindustan Unilever, ITC, or ONGC) make profits, they share a portion with their shareholders. This share is called a dividend. By buying a portfolio of high-dividend-yield stocks, you can generate regular cash flow.

Best Sectors for Dividend Income in 2026

In 2026, PSU (Public Sector Undertaking) banks and Power companies are offering attractive dividends due to government policies. Also, FMCG companies remain consistent dividend payers.

Risks and Rewards of Dividend Investing

- Reward: High potential income (yields of 4-6% plus stock price appreciation).

- Risk: Stock prices fluctuate. The company can skip the dividend if business is bad. Dividends are not guaranteed .

How Much Monthly Income Can You Earn?

To earn ₹20,000 a month (₹2.4 lakh a year) from dividends at a 5% yield, you need an investment of approximately ₹48 lakh in dividend-focused stocks. This is a high-ticket strategy.

Tips for Beginners

Avoid chasing high dividend yields (>8%) as they often come from failing companies (value traps). Look for companies with a track record of 10+ years of consistent dividend payouts.

Suggested SEO Keywords: Best dividend stocks 2026, stock market passive income, high dividend yield shares, monthly dividend income India.

5. Senior Citizen Savings Scheme (SCSS) and Government Schemes

What is SCSS?

The Senior Citizen Savings Scheme (SCSS) is a government-backed retirement savings vehicle. It is the best investment plan for monthly income for anyone over 60 years old. You can invest a lump sum, and you receive interest quarterly .

Government Monthly Income Schemes in 2026

- SCSS: 8.2% per annum (Quarterly Payout) . Max investment: ₹30 lakh.

- Post Office Monthly Income Scheme (POMIS): 7.4% per annum (Monthly Payout). Max investment: ₹9 lakh (Single) / ₹15 lakh (Joint) .

Interest Rates and Safety Benefits

As of the April-June 2026 quarter, the government has kept SCSS interest rates unchanged at 8.2% . This is significantly higher than bank FDs. These schemes are backed by the Government of India (Sovereign Guarantee), meaning there is zero default risk.

Tax Benefits of Government Investment Plans

- SCSS: Investments up to ₹1.5 lakh qualify for deduction under Section 80C. However, the interest earned is fully taxable as per your income slab.

- POMIS: No 80C benefit, but a safe way to get monthly cash.

Best For Retired Investors

If you are a retiree, you can combine SCSS and POMIS to cover your basic living expenses. For example, investing ₹15 lakh in POMIS (Joint) yields ~₹9,250 monthly . Investing ₹20 lakh in SCSS yields ~₹13,600 quarterly (approx ₹4,500 per month on average).

Suggested SEO Keywords: Government investment plans, SCSS scheme 2026, post office monthly income scheme, best retirement investment plans.

Comparison Table of Top Monthly Income Investment Plans in 2026

Best Investment Plan Based on Your Financial Goals

Best for Beginners

Fixed Deposits (FDs) or Post Office MIS. Start with a small amount (₹50,000) to see how monthly payouts feel before committing large sums.

Best for Retirees

Senior Citizen Savings Scheme (SCSS) + POMIS. These offer the highest safety and senior citizen exclusive rates. As of 2026, SCSS gives 8.2%, which is unbeated for risk-free returns .

Best for High Monthly Income

Dividend Stocks or REITs. If you can handle market volatility, these have the potential to generate higher than 10% returns (including capital appreciation).

Best Low-Risk Investment Plan

Bank FD or POMIS. The principal is safe, and the income is fixed, though it may not beat inflation post-tax.

Best Long-Term Wealth Building Option

Mutual Funds SWP. By keeping the money in hybrid funds, your capital continues to grow even while you withdraw a small portion.

Common Mistakes to Avoid While Investing for Monthly Income

Investing Without Research

Do not invest just because your neighbor is investing. A monthly income plan is only good if it fits your timeline. SCSS requires a 5-year lock-in; if you need money in 2 years, an FD is better.

Ignoring Inflation

A fixed income of ₹10,000 today will be worth much less in 10 years. Do not put all your money into fixed-income products (like FDs or POMIS). Allocate at least 20-30% to equity or hybrid funds to keep your income growing with time .

Choosing High Returns Without Understanding Risks

If someone promises you 15% “safe” monthly income, run away. These are usually Ponzi schemes. Stick to registered SEBI/RBI products.

Not Diversifying Investments

Never put all your ₹1 crore into one SCSS account or one stock. Divide your money across 3-4 different assets to balance the risk of one failing.

Expert Tips to Build Passive Monthly Income in 2026

Diversify Your Portfolio

Create a “Laddering” strategy. For example: ₹5 lakh in POMIS for base safety, ₹5 lakh in SWP for tax-free growth, and ₹5 lakh in REITs for high yield.

Start SIPs Early

If you are young, do not wait for retirement. Start a SIP in a Nifty 50 Index Fund today. After 15 years, you can convert that large corpus into a SWP to generate massive monthly income .

Reinvest Extra Earnings

If you don’t need the monthly income immediately, reinvest it. In 2026, many digital apps allow “Auto-Invest” features to put your interest back into the market, using the power of compounding.

Track Investment Performance Regularly

Interest rates change. For example, SCSS rates might change next quarter (reviewed by the government on June 30, 2026) . Review your portfolio every 6 months to ensure you are getting the best rates.

FAQs About Investment Plans for Monthly Income in 2026

Which investment gives the highest monthly income in 2026?

Stock market-linked instruments like Dividend Stocks and SWP generally give the highest returns (8-12%), but they carry market risk. For guaranteed returns, SCSS offers the highest (8.2%) .

What is the safest investment plan for monthly income?

The Post Office Monthly Income Scheme (POMIS) and SCSS are the safest because they are backed by the Government of India. They offer fixed, guaranteed returns without market fluctuation.

Can I get monthly income from mutual funds?

Yes, by setting up a Systematic Withdrawal Plan (SWP) . You can withdraw a fixed amount from a mutual fund every month. However, if the market crashes, your principal might get depleted .

Are dividend stocks good for passive income?

Yes, but they should not be your only source. Dividends are not guaranteed. However, top dividend-paying stocks like ITC, Hindustan Unilever, and Coal India have historically provided consistent payouts for decades.

Which investment is best for retirees in India in 2026?

The Senior Citizen Savings Scheme (SCSS) is unequivocally the best due to the 8.2% interest rate and 80C tax benefit. Pair it with a Senior Citizen FD for better liquidity .

How much money is needed to earn ₹50,000 monthly income?

It depends on the yield.

- Using SCSS (8.2%) : You need approx ₹73 lakh (since payout is quarterly, adjust accordingly).

- Using Bank FD (7%) : You need approx ₹85 lakh.

- Using SWP (9%) : You need approx ₹66 lakh (depending on market conditions).

Conclusion

Generating a steady monthly income in 2026 is achievable if you balance safety and growth. The Top 5 Investment Plans—SWP Mutual Funds, Monthly Income FDs, Real Estate/REITs, Dividend Stocks, and Government Schemes—each solve different problems.

- If you are over 60, stick to SCSS and POMIS for worry-free cash .

- If you are in your 40s, use SWP to create a second salary.

- If you have high capital, REITs offer the best inflation-beating rental income.

Start by calculating your monthly expense target, decide your risk profile, and build a diversified portfolio. Remember, the best time to start your monthly income investment plan was yesterday; the second best time is today.